Before the Explosion of the $8 Billion Robotics Market: Opportunities for the Chinese Supply Chain in Saudi Arabia (Part 1)

The Window is Open – Your Guide to Breaking Through is Loading

Saudi Arabia's purchase orders are already issued. The key is how to deliver them safely.

For many, humanoid robots are still a "future concept," expected to land first in the US, Japan, or South Korea. But the reality is that the earliest real buyers are emerging elsewhere - Saudi Arabia.

Not out of curiosity, but because they are wealthy, have urgent needs, and lack the patience to wait for regulations to slowly mature.

In 2024, while global tech companies were still debugging humanoid robots in labs, Saudi Arabia's Public Investment Fund (PIF) announced a $100 billion investment in AI and robotics. The NEOM project explicitly stated its goal to deploy 100,000 service robots by 2030.

This is not an exhibition, not a proof of concept. These are real purchase orders backed by real money.

But while the opportunity is there, the path forward is not simple. The core components of humanoid robots - AI vision algorithms, motion control systems, high-performance sensors - are almost all on the U.S. export control list.

Exporting finished products? Customs seizures, Entity List risks, re-export tracing – any of these can turn an order into nothing. The companies that will truly capture this market are not necessarily the most technologically advanced or the strongest brands, but those capable of providing a complete solution: "Robot + Compliance Pathway + Local Delivery."

01 Saudi Arabia's Rigid Demand: Why Now?

Saudi Arabia's demand for robots stems not from tech enthusiasm, but from the rigid pressures of its national strategy.

The Vision 2030 plan aims to increase non-oil revenue's share of GDP from 16% to 50% by 2030. This requires large-scale development of labor-intensive industries like tourism, logistics, manufacturing, and healthcare.

The problem: Saudi Arabia's local workforce is only 14 million, with 60% employed in the government sector. The private sector relies heavily on expatriate labor.

Data from 2023 shows that expatriates account for as much as 77% of the private sector workforce in Saudi Arabia. In industries like construction, logistics, and hospitality, this ratio exceeds 90%. However, since 2021, the Saudi government has been enforcing a "Saudization" policy, requiring companies to gradually increase the proportion of Saudi nationals in their workforce, while simultaneously raising visa fees and levies for expatriate workers.

The annual cost for an expatriate construction worker has risen from approximately $12,000 in 2020 to $25,000 in 2024, an increase of over 100%. Faced with the triple pressures of labor shortages, soaring costs, and localization mandates, automation has become the only viable path.

NEOM, Saudi Arabia's $500 billion "future city" on the Red Sea coast, spans 26,500 square kilometers and is planned to accommodate 9 million residents. According to official NEOM project documents, the goal is to achieve a 1:3 human-to-robot ratio - that is, one service robot for every three people.

The initial project phase (2024-2025) has already specified the deployment of 100,000 robots in scenarios like airports, hotels, logistics centers, and construction sites.

These 100,000 robots are not toys; they are meant to be genuine labor substitutes:

- High-risk tasks at construction sites: material handling, welding, spraying

- Logistics centers: sorting,mobilization, inventory management

- Hotels and malls: reception, cleaning, food delivery, security

- Healthcare facilities: patient guidance, dispensing medication, disinfection,company

NEOM's timeline is aggressive: Complete initial infrastructure by end of 2024, begin large-scale robot deployment in 2025, welcome first residents in 2026. This means 2024-2025 is the golden window for robotics suppliers. Miss it, and you'll face fiercer competition and tougher terms.

According to the International Federation of Robotics and Statista data, the Saudi robotics market is projected to grow from $1.5 billion in 2023 to $8 billion by 2030, a compound annual growth rate (CAGR) of 28% - more than double the global average.

This $8 billion is highly concentrated in several key sectors: Service robots ($3.5 billion, 44%), Construction robots ($2.0 billion, 25%), Logistics robots ($1.5 billion, 19%), and Industrial robots ($1.0 billion, 12%).

Crucially, this market isn't forming spontaneously; it is government-led, financially backed, and project-driven.

02 The Real Buyers: Who Controls the Saudi Robotics Market?

The real buyers in the Saudi robotics market are not startups or tech parks, but government-backed investment funds and project operators.

The Saudi Public Investment Fund (PIF) is the world's fifth-largest sovereign wealth fund, managing over $700 billion in assets. In 2024, PIF announced the creation of a dedicated AI and Robotics investment division, with an initial allocation of $100 billion focused on humanoid and service robot companies, the core components supply chain, and building local robot assembly and integration capabilities.

PIF's investments are not purely financial; they are strategic procurement coupled with technology transfer. They typically require invested companies to establish local assembly plants in Saudi Arabia, train local engineers, and transfer some technology patents.

Although the funds come from the government, actual procurement decisions are often made by EPC (Engineering, Procurement, and Construction) contractors. Mega projects like NEOM, the Red Sea Project, and Qiddiya are contracted out to local Saudi EPC firms, which manage the entire process from design to delivery.

Major Saudi EPC players include: Saudi Binladin Group (largest construction group, contractor for multiple NEOM sub-projects); ACWA Power (energy and infrastructure giant, handling NEOM's clean energy and smart grids); Saudi Aramco Engineering (Aramco's engineering subsidiary, involved in industrial automation projects).

The procurement logic of these EPC firms differs from government funds:

- Greater focus on delivery certainty:Can you deliver on time? Provide on-site commissioning? Offer localized services?

- Greater focus on total cost of ownership (TCO):Looking beyond the purchase price to maintenance costs, spare parts availability, and upgrade capabilities.

- Greater focus on compliance:Can goods clear customs smoothly? Are there sanctions risks? Do they meet local Saudi standards?

A Chinese engineer with years of experience in Saudi Arabia told us: "What EPC companies fear most is a supplier 'disappearing' after the sale. They'd rather pay 20% more to secure a supplier offering a 10-year maintenance commitment. So for Chinese companies to win orders, they absolutely must establish a local service team in Saudi Arabia. You can't just 'sell and run.”

Beyond government funds and EPC firms, another category of buyers includes operators of specific venues. Saudi Arabia plans to increase its annual passenger throughput from 100 million to 330 million by 2030. Projects like the new Riyadh airport and the Jeddah airport expansion explicitly require the integration of service robots.

Saudi Arabia is building itself into a Middle Eastern logistics hub, attracting global logistics giants like Amazon, DHL, and SF Express to establish regional centers, all of which require extensive automation equipment.

The key difference between Saudi and Western buyers: They aren't looking to "try it out"; they are looking to "deploy immediately." The typical procurement process for a Western company involves 3-6 months for proof of concept, 6-12 months for a small-scale pilot, 3-6 months for ROI evaluation, and 12-24 months for scaled-up deployment – a total of 2-3 years.

The Saudi buyer's process is: 1 month to define requirements, 1-2 months to screen suppliers, 1-2 months to negotiate and sign contracts, and 3-6 months for direct deployment. From requirement to deployment, it can be done in as little as 6 months.

03 Compliance Challenges: Why Finished Product Exports Won't Work

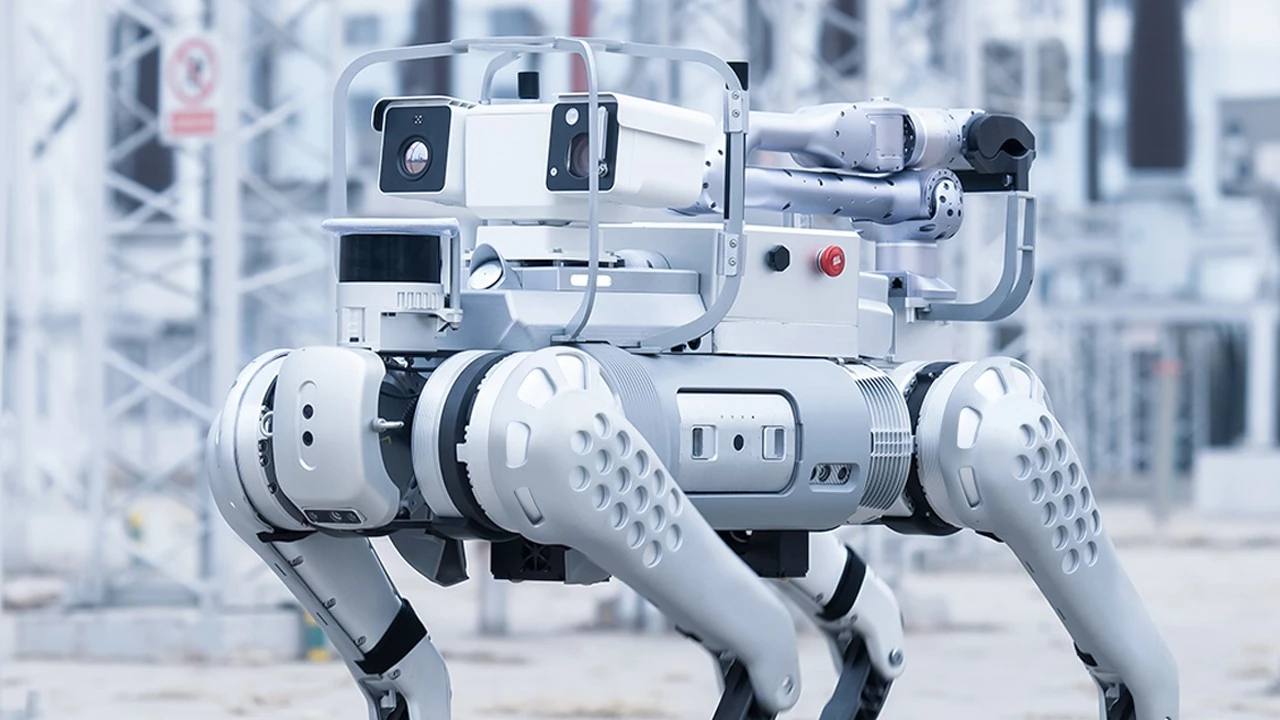

Humanoid robots may look like "consumer electronics," but on export control lists, many of their core components are considered sensitive technologies.

The U.S. Department of Commerce's Bureau of Industry and Security (BIS) Export Administration Regulations (EAR) classify commodities and technologies under different Export Control Classification Numbers (ECCNs). Sensitive classifications relevant to humanoid robots include:

- ECCN 3A001(Electronics): Includes high-performance image sensors, LiDAR modules, inertial measurement units (IMUs).

- ECCN 4A003(Computers): Includes AI inference chips, edge computing modules, neural network accelerators.

- ECCN 4D001 and 4E001(Software and Technology): Includes computer vision algorithms, path planning and navigation software, human-machine interaction systems.

If a humanoid robot contains components or technology covered by these ECCNs, exporting it to Saudi Arabia requires a BIS license. The application process typically takes 3-6 months, and the approval rate is less than 50%. Even if approved, it may come with strict end-user restrictions and re-export tracing requirements.

Complicating matters further, the U.S. has additional scrutiny for Chinese companies. In 2024, the U.S. added several Chinese AI and robotics companies to the Entity List, including SenseTime, DJI, Hikvision, and iFlytek.

If a humanoid robot uses technology or components from these listed companies, the export could be denied even if the robot manufacturer itself is not on the list.

The EU's Dual-Use Regulation also imposes hurdles on robotics exports. While EU controls on China are relatively looser, exports to the Middle East require additional scrutiny due to concerns about technology diversion to sanctioned countries like Iran.

In practice, EU customs randomly inspects high-tech products "Made in China, destined for the Middle East." If undeclared sensitive components are found, the goods are seized, and the company faces fines or even blacklisting.

Japan's Ministry of Economy, Trade and Industry (METI) also strictly controls the export of core robotics components, especially servo motors and reducers. Japanese companies dominate the global high-end servo system market. Exporting these products to China already requires end-user certificates. If a Chinese company then re-exports them to the Middle East, it must apply for re-export permission from the Japanese government.

Even if export is theoretically possible, practical risks like customs seizure remain. In 2023, an industrial robot company in Shenzhen exported welding robots to the UAE.

During declaration at Shenzhen customs, they were required to provide supplementary explanations regarding the source of the robot's AI algorithms, the chip models in the vision system, and the end-user information. It took the company two weeks to provide the materials. Ultimately, customs ruled it involved "sensitive technologies" and required the company to apply for a dual-use export license.

The license approval took another three months, during which the goods remained warehoused, and the client nearly canceled the order.

Facing these compliance barriers, how can Chinese companies break through? Three proven export pathways will be detailed in Part 2.

November 26-28, the World Trade Expo Saudi will be held in Jeddah, Saudi Arabia. We have strategically positioned ourselves in three hot sectors - Robotics, New Energy, and E-sports - building a bridge for Chinese companies to directly access the Saudi market. Follow our official account for practical guides.